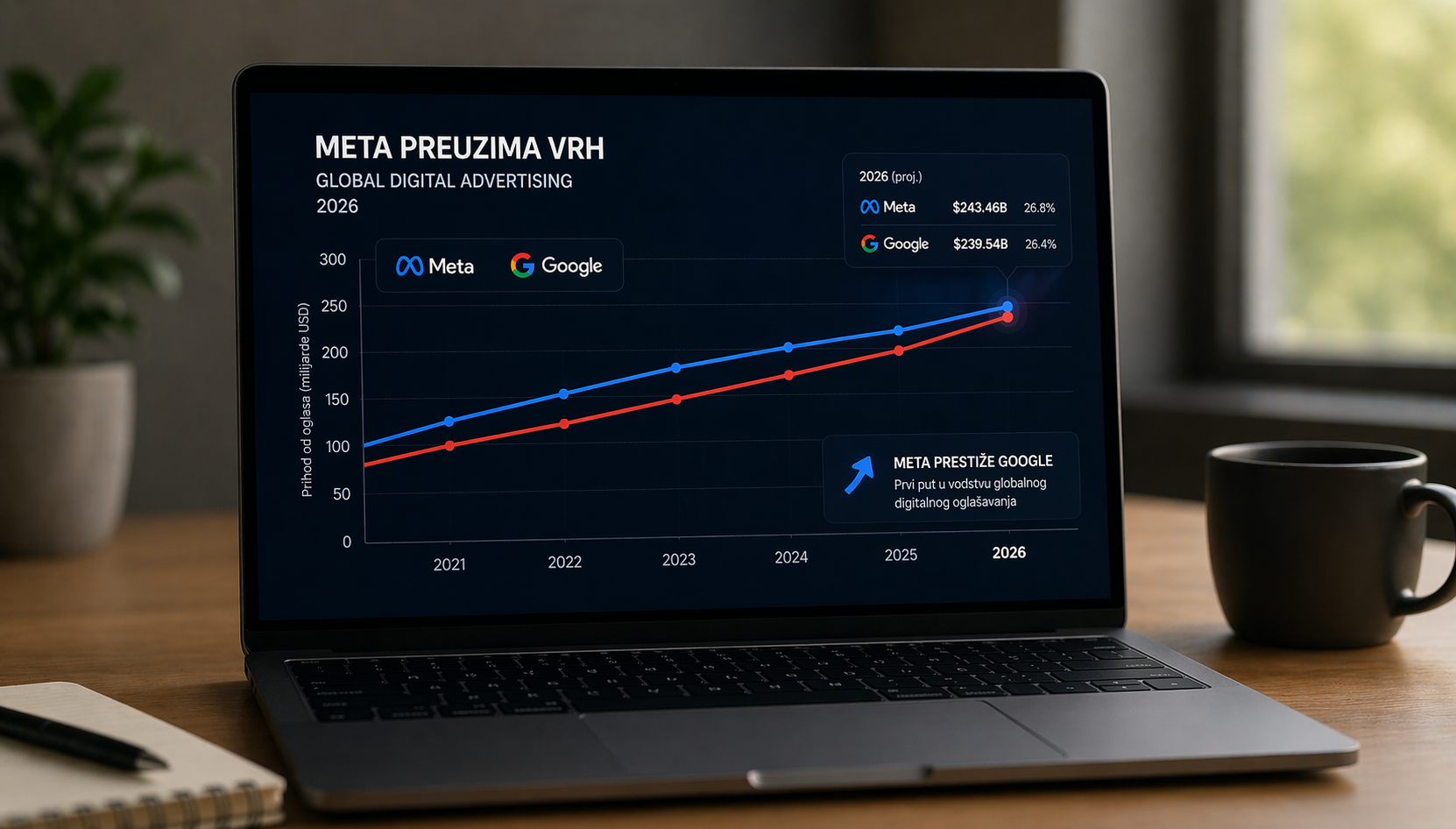

Meta Platforms could achieve what until recently seemed unlikely in 2026 and take the leading position in global digital advertising from Google. According to estimates by Emarketer, this is a symbolic but important moment that shows how the balance of power in the market is shifting.

Meta is expected to reach $243.46 billion in ad revenue this year and a 26.8% global share, while Google is projected at $239.54 billion and 26.4%. The gap is not large, but it is significant because it comes after a long period in which Google consistently held the leading position.

The shift is not the result of a single product or a short-term impulse, but of continuous growth across the entire Meta ecosystem. The company is simultaneously increasing the efficiency of existing channels and opening new ones, with automation and AI tools playing a key role by directly impacting campaign performance.

It is precisely this combination of better targeting, real-time optimisation and simpler campaign management that makes Meta’s platforms increasingly attractive to advertisers. This is clearly reflected in growth rates. Meta accelerates to 24.1% in 2026, while Google remains at 11.9%. The difference in momentum becomes more important than the size of the companies themselves, as it ultimately determines the distribution of market share. In other words, Meta is not taking the lead suddenly, but catching up through consistently faster scaling.

A significant part of this growth comes from formats aligned with current user behaviour. Reels, as a response to the dominance of short-form video, is attracting increasing budgets while also strengthening overall engagement on platforms such as Facebook and Instagram. At the same time, the expansion of advertising capabilities on WhatsApp and Threads further increases monetisation opportunities without relying on a single channel.

On the other hand, Google remains extremely strong, particularly in the search segment. However, its revenue structure is broader, with a significant share coming from subscription services such as YouTube Premium, which affects the overall dynamics of advertising growth. In addition, changes in how users access information, including the rise of AI tools and alternative search formats, are gradually reshaping the context in which search advertising operates.

This shift at the top does not indicate market fragmentation, but the opposite. Digital budgets continue to concentrate around a few major platforms. Alongside Meta and Google, Amazon holds a stable third position with around a 9% global share. Together, these three companies control more than 62% of total digital ad spend, clearly demonstrating how centralised the market is.

Behind them are ByteDance, Microsoft and Apple, but with significantly smaller shares. This creates an environment in which smaller players find it increasingly difficult to compete on the basis of technology, data and reach, making them the first to be affected when budgets are reduced or market instability arises.

Despite growing regulatory pressure and legal challenges, estimates suggest that these factors do not yet have a decisive impact on budget allocation. Advertisers continue to make decisions primarily based on performance, further reinforcing the positions of platforms that can deliver measurable results at scale.

Ultimately, this shift is not only about who is first, but about how the logic of digital advertising is changing. Advantage no longer comes from a single innovation, but from the ability to connect data, distribution and automation into a system that continuously delivers better results. In that model, Meta currently holds a slight but critical advantage.